Military Appreciation Month is celebrated each year in May. This recognition was designated by Congress in 1999, allowing us to use the month to celebrate and pay tribute to those who have sacrificed so much for our freedoms. To acknowledge this recognition, we are highlighting and detailing the benefits and features of Veteran Affairs (“VA”) loans.

What is a VA Loan?

A VA loan is a mortgage option issued by private lenders and partially backed by the Department of Veterans Affairs. For many military borrowers, this specific type of loan can be extremely helpful and beneficial. Let us break this down and explain why.

What Are Some VA Loan Features & Benefits?

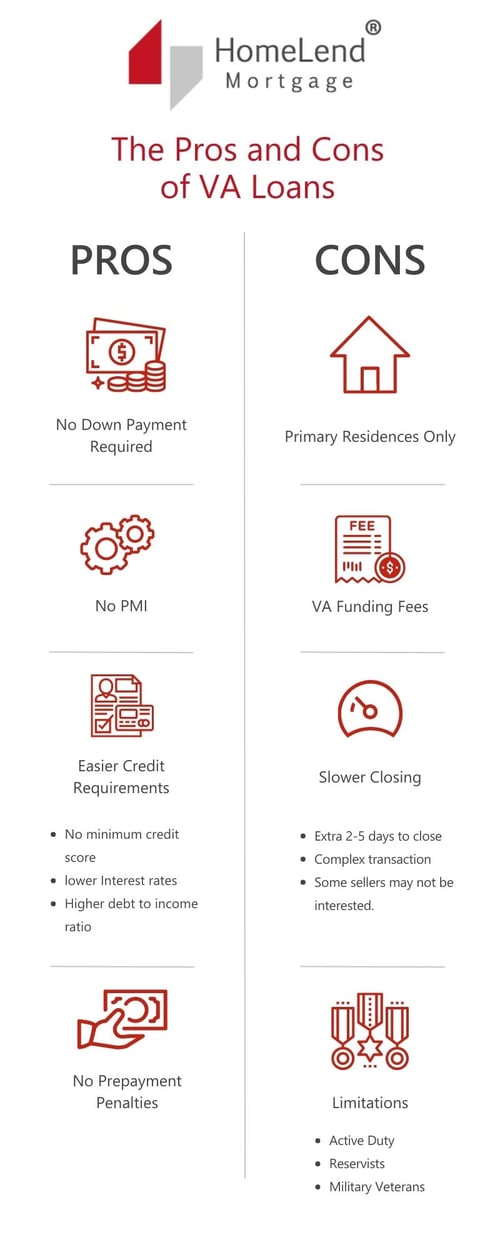

- No down payment required.1

- Competitively low interest rates.

- No need for Mortgage Insurance (MI). Not having to pay MI can save a borrower on their monthly mortgage payment. 2

- The VA home loan is a lifetime benefit. Once you have earned and qualified for eligibility of a VA loan, it will never expire.

Who Qualifies For A VA Loan?

If you are a Servicemember, Veteran, or an eligible surviving spouse, taking advantage of a VA Loan could be an excellent option for your home buying needs. The VA Guaranteed Home Loan program was created by the original G.I Bill, Servicemen’s Readjustment Act of 1994, originated to support Veterans and Veteran families after their homecoming. Active members may include those who have served ninety (90) continuous days, Veterans who have met the length of service requirements (typically 90 days during wartime and 181 days during peacetime), those that have completed 90 days active-duty service or six creditable years in the Selected Reserve/National Guard, or if you are a surviving spouse of a Veteran. Still, there are other ways to qualify if an individual does not meet the preceding requirements; best practice is to check with the VA for comprehensive details.

What Are Four Things Borrowers Wouldn’t Know About VA Loans?

- VA Loans are reusable, depending on your circumstances. For example, providing you pay off your prior VA mortgage and you no longer own the property. Or on a one-time only basis, eligibility for a loan can be restored providing your VA loan has been paid in full and you still own the property.

- Qualified borrowers can borrow as much as a lender is able to provide them with. VA loan limits are higher in 2022 because of rising home prices. VA loan limits match those set by the Federal Housing Finance Agency on confirming loans. They do not cap the amount you can borrow; they set the maximum you can finance for no money down. See the VA loan limit in your county, for borrowers to whom limits still apply.

- There are no prepayment penalties. Borrowers can make payments at any time, potentially saving a significant dollar amount in interest for the loan.

- When considering a VA loan, lenders are required to examine a borrower's comprehensive loan profile. As such, the VA does not have a minimum credit score requirement.

Summary

Purchasing a new home is one of life's biggest, most exciting milestones – which can also be an incredibly daunting process. We are here to make getting a mortgage easy and enjoyable, offering our best-in-class, personalized assistance. Our mortgage loan programs are created to help you achieve your unique financial goals. Regardless of where you are on your financial journey – we salute you and we are here to make your dream of homeownership a reality.

This information is for informational purposes only and is intended to provide general guidance and does not constitute legal, tax, or financial advice. Each person’s circumstances are different and may not apply to the specific information provided. You should seek the advice of a financial professional, tax consultant, and/or legal counsel to discuss your specific needs before making any financial or other commitments regarding the matters related to your condition are made.

References:

- https://www.benefits.va.gov/homeloans/

- https://www.veteransunited.com/valoans/10-things-many-borrowers-dont-know-about-va-loans/

- https://www.nerdwallet.com/article/mortgages/va-loan-eligibility-requirements

- https://time.com/nextadvisor/mortgages/va-loan-limits/

- https://www.benefits.va.gov/homeloans/faq_eligibility.asp#:~:text=Q%3A%20I%20have%20already%20obtained,eligibility%20restored%20for%20additional%20use.

- https://www.bankrate.com/mortgages/va-loan-requirements/

- https://blogs.va.gov/VAntage/31825/ten-things-veterans-dont-know-va-home-loans/

Disclosures:

- Some lenders may require down payments for some borrowers using the VA home loan guarantee, however, VA does not require a down payment.

- Mortgage Insurance is a type of insurance that protects the lender if the borrower does not pay the mortgage obligation. It is usually required on conventional loans if the down payment is less than 20% of the total mortgage amount. Mortgage Insurance Premium (“MIP”) is what the Federal Housing Administration (FHA) requires borrowers to pay to self-insure an FHA loan against future loss.